Achieving financial freedom is not based on luck. There is a process to follow in order for us to reach this goal. That’s why we all need a solid financial plan.

There are levels that we need to go through. The lower levels need to be addressed first before jumping to the higher ones.

It’s like building a house. We can’t put the roof yet without building first the walls and the foundation.

If we start with the roof or the walls, sooner or later it will fall and will definitely be a disaster.

Wealthy people follow a financial plan more or less similar to what is mentioned in this post. It’s time for us future wealthy people to apply one too.

As a member of the International Marketing Group (IMG), I learned that our solid financial plan should look like this:

We must build our financial plan in this order:

HEALTHCARE

this will cover our medical expenses when we get sick during our working age and when we eventually retire

short-term healthcare – provided by our employers while we are employed but stops when we resign, terminated or retire

long-term healthcare – medical expenses coverage during our retirement age

PROTECTION

in case something happens to us (death or disability), our families would receive a certain amount of funds to cover our inability to earn income

this is addressed by getting a life, disability or income protection insurance

ELIMINATE DEBT

We can’t afford to invest if we are burdened with debt. We must settle and eliminate our debt first.

If our debts are interest-bearing, the interest will just eat up both our funds and the potential gains from our investments

It is not advisable to borrow money for investment.

EMERGENCY FUND

reserved funds to cover our unexpected expenses during emergencies like disasters and job loss

must be at least 3 to 6 months of our income, if we are earning P10,000 per month then we need to have at least P30,000 to P60,000 set aside as our emergency fund

must be kept in a readily accessible bank account

INVESTMENTS

The first 4 steps should be addressed first before investing.

You can invest in mutual funds, stocks or real estate

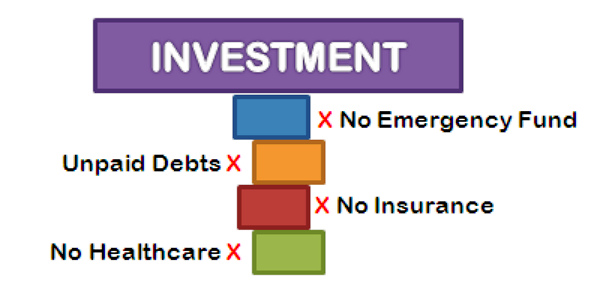

Most of us, new investors, would go straight to investments. We get blindsided by the high rate of return of investing in stocks or the opportunity to own real estate. We don’t bother to go through the lower levels.

Highly likely most new investors have most of their saved money in stocks, mutual funds or real estate investments. Their financial picture look like this:

Going directly to investments means a financial disaster waiting to happen.

If you get sick and hospitalized, you just can’t show your stock certificate, mutual fund statement or contract to sell to the hospital.

The most likely thing you’ll do is to withdraw or sell your investments to pay off your medical expenses.

What if the stock market is down or you haven’t fully paid your real estate investment?

It’s either you give up your investment at a loss or you borrow money just to cover your hospital bills.

This is when you appreciate the importance of having a health insurance. Instantly, you’ll have funds to cover your medical expenses without giving up your investment.

The same scenario happens if an emergency arise or something bad happens to you. Putting most or all of our money in investments is definitely not a good move.

I admit that when I started investing, most of my funds are heavily invested in real estate and I had a similar financial picture above.

I did not know about building a solid financial foundation. What I only cared about is how to invest my money safely.

When I joined the International Marketing Group (IMG), I learned that achieving financial freedom takes time and there are no short cuts. We all must go through a process.

At the moment, I am slowly correcting and building the base of my financial foundation.

I am setting aside some money each pay day to the bank to serve as my emergency fund. So far my emergency fund is almost equivalent to 3 months.

I also have my Kaiser healthcare which I pay every month to cover my medical expenses when I get hospitalized or retire, or even if I don’t use it, I can withdraw the increased cash value of what I paid in the future. Kaiser also serves as my life and disability insurance if something happens to me. Definitely a 3-in-1 investment product.

With regards to debts? I am allergic to credit cards and loans that’s why I don’t worry about them yet. I try to live a simple, content and frugal lifestyle.

With me addressing the lower levels, it’s just natural that money set aside for my stock and mutual fund investment to also decrease. But it doesn’t matter because I know that if unexpected things happen, I got myself and my family financially covered.

To read my posts about the individual levels of investing, you can visit the links below:

Level 1: Healthcare+Life Insurance+Retirement Fund through Kaiser (please read: LEVEL 1 INVESTING: KAISER HEALTHCARE)

Level 2: Mutual Funds (please read: LEVEL 2 INVESTING: MUTUAL FUNDS)

Level 3: Stocks (please read: LINK COMING SOON)

Level 4: Real Estate (please read: LINK COMING SOON)

Feel free to also leave a comment or to send me a personal message if you have other questions, here: gladys.img.trulyrichmakers@gmail.com

Thanks for sharing the information. That’s a awesome article you posted. I found the post very useful as well as interesting. I will come back to read some more scheme

ReplyDeleteGreat information thanks for sharing

ReplyDeleteFMCG shares

Nifty FMCG

Hey...Great information thanks for sharing such a valuable information

ReplyDeleteMotilal Oswal Asset Management

ReplyDeleteHey...Great information thanks for sharing such a valuable information

Siemens Limited shares

ROE

Hey...Great information thanks for sharing such a valuable information. you may also check our blog.

ReplyDeleteMahindra & Mahindra Financial

Mahindra & Mahindra Financial Shares